Rating: SELL

STRONG SELL (5-tier) · quality defensive · conviction: medium

| Metric | Value |

|---|---|

| Current Price | $113 |

| Triangulated Fair Value | $67 (-40% vs spot · triangulated FV) |

| 12-mo Scenario PWEV | $79 (-30% vs spot · 12m PWEV) |

| Forward P/E | 58.8x |

| Market Cap | $90B |

| 52-Week Range | $64–$154 |

EPS basis for the forward P/E and all scenario multiples: consensus forward EPS (broker-adjusted, non-GAAP).

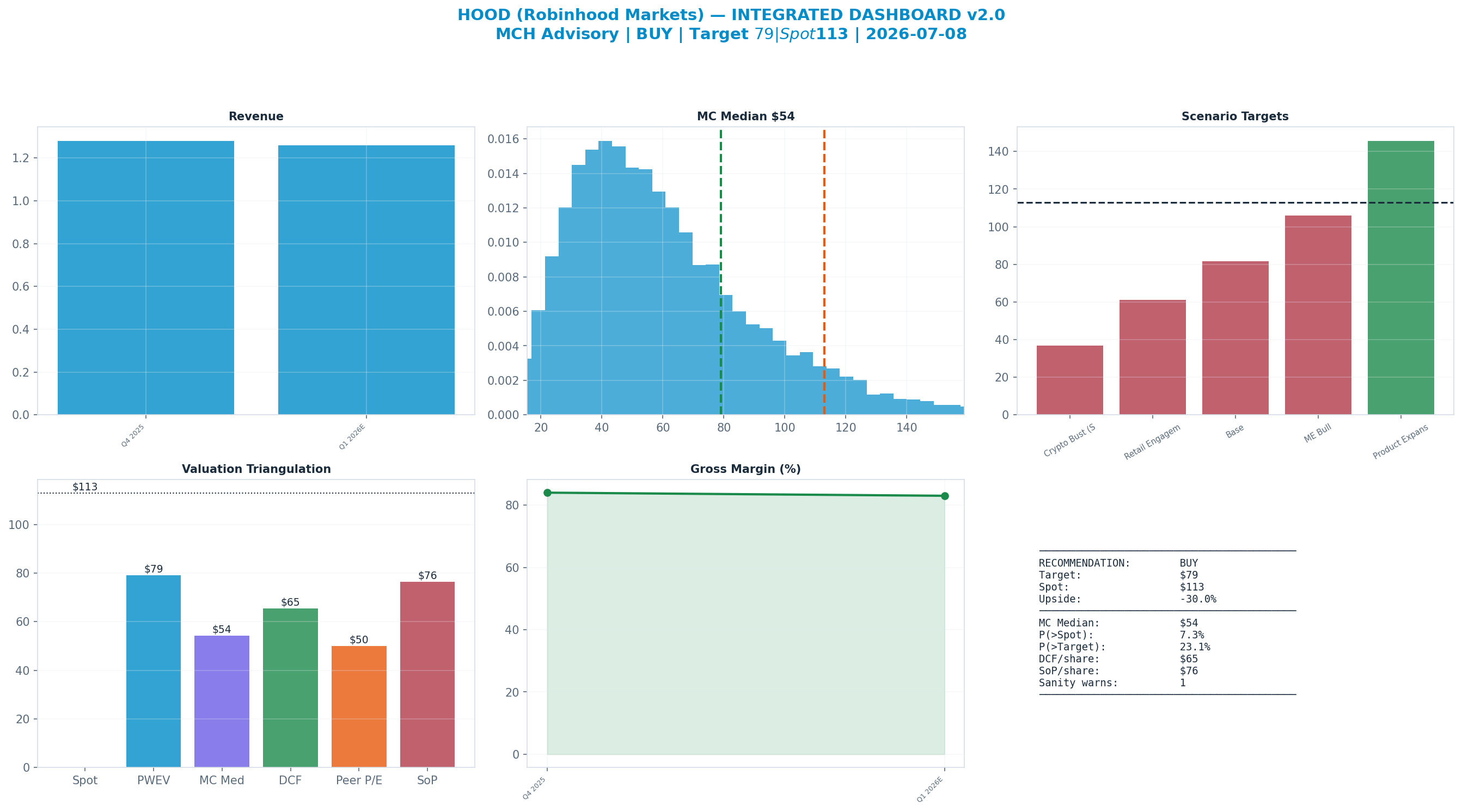

Methodology: Valuation triangulated across five independent anchors — Monte Carlo (Student-t + regime switching), an independent DCF, peer re-rating, a sum-of-parts, and a scenario-weighted PWEV. Figures reconciled to mch_weekly_run live prices. Each chart below sits with the part of the thesis it evidences.

General research for a skeptical institutional reader. Not personalised investment advice; no position sizing or trade instructions. Figures as of the analysis date; verify before acting.

Investment Committee Summary

| Rating | SELL · STRONG SELL (5-tier) |

| Classification · conviction | quality defensive · medium |

| Triangulated fair value | $67 (-40% vs spot · triangulated FV) |

| 12-mo scenario PWEV | $79 (-30% vs spot · 12m PWEV) |

| Next catalyst | 2026-07-29 — Quarterly earnings |

| Primary thesis-break | Crypto transaction revenue, YoY < -30% (2 consecutive prints) |

📎 Download the full model (Excel) — DCF line items, scenarios, sensitivity, assumptions, and extended fundamentals.

Rating Bridge

Rating = SELL because:

- Probability-weighted scenario value implies -30% vs spot

- Monte Carlo median implies -52% vs spot

- DCF fair value implies -42% vs spot — but this is terminal-value sensitive (exit-multiple $65 vs Gordon $50, 24% apart), so it carries less weight

- Bear case (Crypto Bust (Structural)) downside is -67% vs spot

- Net: reward/risk of 0.6× warrants a Sell.

Investment Thesis

At $100 spot on a ~52x forward multiple, the market is paying for HOOD to compound funded accounts and ARPU through a durable product cycle — treating the 2021-22 boom-bust as history rather than the operating template. The engine disputes that. The probability-weighted target of $79 sits ~21% below spot because the multiple, not earnings, carries the valuation: variance decomposition attributes ~84% of outcome dispersion to the P/E, and only ~16% to growth and margin combined. Our five-scenario segment build yields EPS of roughly $2.04 to $3.55, and the range of fair values ($40 to $150) turns almost entirely on whether the market keeps paying a growth multiple or de-rates toward the 18-31x brokerage band. We anchor the rating to that de-rate risk: peers (SCHW, IBKR) trade at 20-22x, and HOOD's transaction lines remain ~50-55% of revenue and acutely cyclical. The single most damaging risk is a simultaneous crypto-volume collapse and a PFOF or crypto-listing regulatory ruling, which hits two transaction lines and the multiple at once.

The dashboard below is the whole argument on one page: spot ($113) against each valuation anchor, the scenario tree, technicals and the options-implied move.

Anti-Thesis (The Real Bear Case)

The steelman for the highest-probability bear — the Base case de-rating toward Crypto Bust — is straightforward mechanics, not pessimism. Roughly half of revenue sits in transaction lines whose volume and take-rate move with retail speculation, and 2022 already demonstrated a >50% year-on-year transaction-revenue collapse. If crypto enters a multi-quarter winter while equities trade a flat-vol tape, both transaction lines compress together while ARPU falls and funded-account growth stalls. NII cushions but cannot offset a correlated hit. The market then re-rates HOOD to a brokerage-like 18x on the view that fintech growth was a cycle, not a trajectory — pushing the target below the 52-week low of $63.52. That is a structural impairment, and its base rate is not trivial.

Key Debate

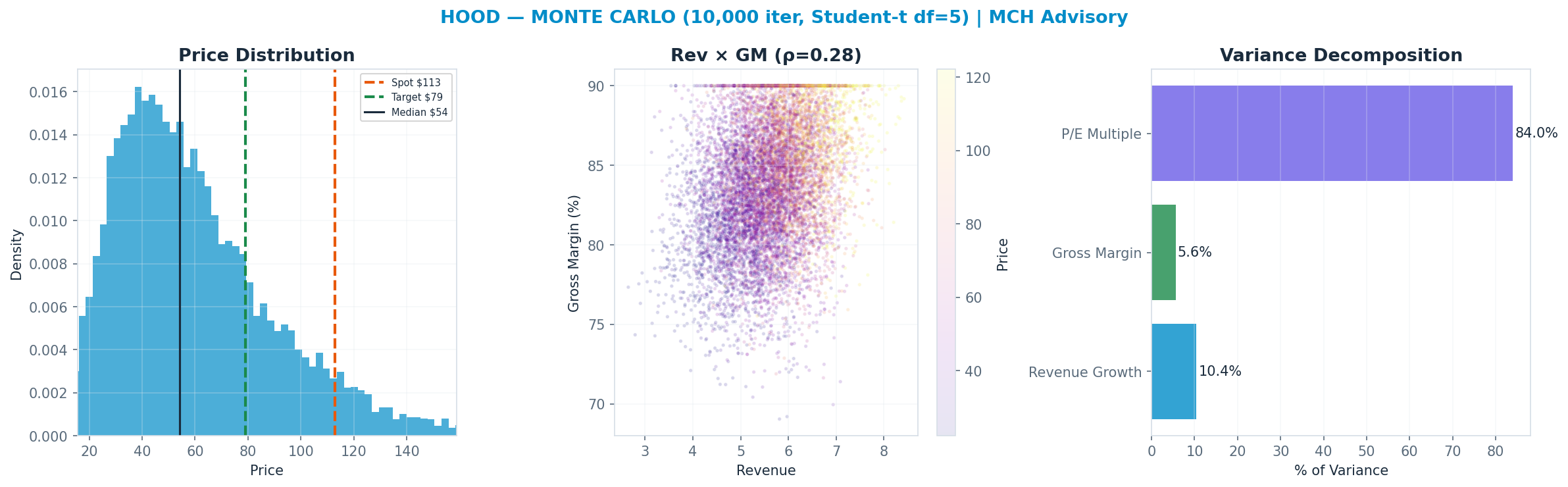

P/E Multiple explains 84% of Monte Carlo outcome variance — i.e. value is set by the multiple the market will pay, a rate/sentiment regime bet as much as an earnings bet.

Earnings-Call Disconfirmation & Sentiment

Derived signals from the MCH market-data store (Alpha Vantage transcripts + news). Quantitative tone only — a disconfirmation flag, not a substitute for reading the call.

Management vs analyst tone (2026Q1): management +0.24 vs analyst floor +0.00 → delta +0.24 (n=63 mgmt / 19 Q&A; 20th pctile across the S&P book, z -0.9).

Flag: TYPICAL — management-vs-analyst tone within the normal cross-sectional range.

| Quarter | Mgmt | Analyst | Delta |

|---|---|---|---|

| 2026Q1 | +0.24 | +0.00 | +0.24 |

| 2025Q4 | +0.40 | +0.18 | +0.21 |

| 2025Q3 | +0.35 | +0.02 | +0.33 |

| 2025Q2 | +0.48 | +0.22 | +0.26 |

News (last 365d, 216 articles): avg ticker sentiment +0.09 (bullish 12% / bearish 3%)

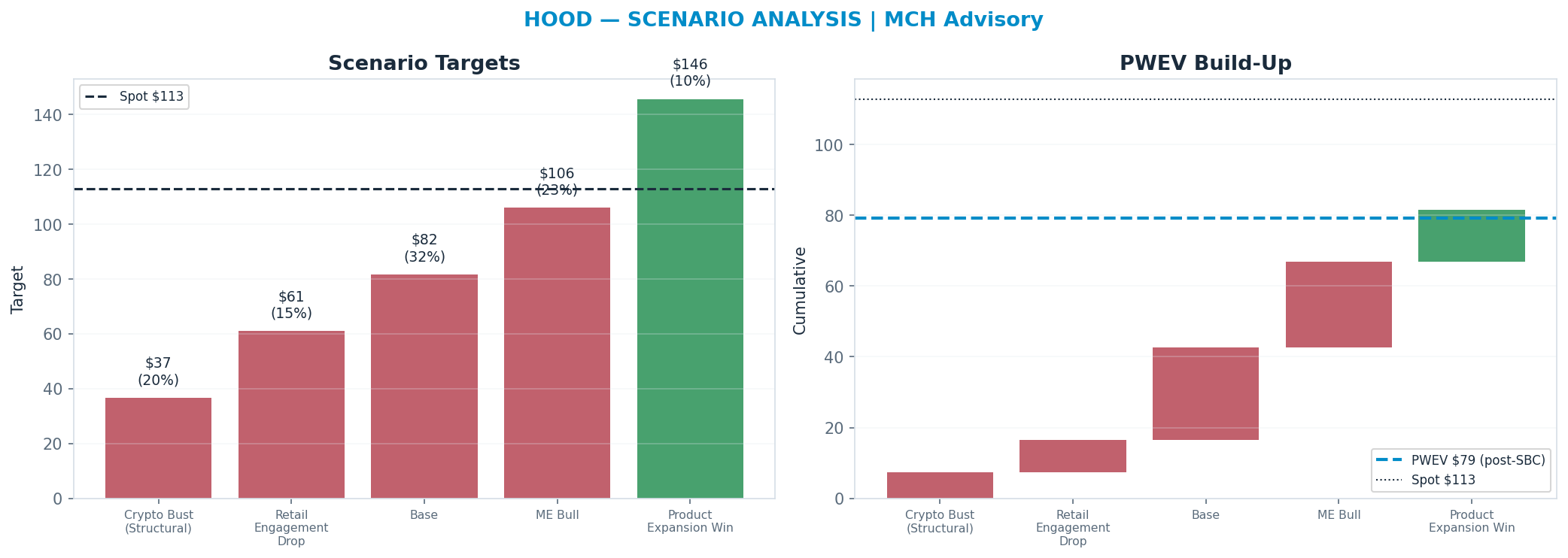

Scenario Analysis

The tree runs from a structural 'Crypto Bust (Structural)' downside ($37) to a 'Product Expansion Win' bull case ($146); the probability-weighted blend (PWEV $79) is -30% versus spot.

| Scenario | Probability | Target | Return vs spot |

|---|---|---|---|

| Crypto Bust (Structural) | 20% | $37 | -67% |

| Retail Engagement Drop | 15% | $61 | -46% |

| Base | 32% | $82 | -28% |

| ME Bull | 23% | $106 | -6% |

| Product Expansion Win | 10% | $146 | +29% |

| Probability-Weighted (PWEV, after SBC dilution) | — | $79 | -30% |

SBC charge: scenario targets are gross per-share prices; the PWEV is reduced by one year of stock-based-compensation dilution (3.0% of shares, on SBC ≈ 10% of revenue), trimming the gross PWEV of $82 to $79 (-2.9%). SBC is charged once, as dilution — never also deducted from FCF.

Scenario rationale — what each probability buys (the driver path behind every target):

- Crypto Bust (Structural) (20%, $37). A multi-quarter crypto winter collapses crypto transaction volume and take-rate, and a quiet equity tape drags options/equities revenue alongside — transaction revenue falls 40%+ as in 2022. Funded-account growth stalls and ARPU compresses as the most active cohort goes dormant; NII cushions but cannot offset. The multiple de-rates to a brokerage-like level on the view that fintech growth was a cycle, not a structural trajectory; the target sits below the 52-week low — a genuine structural impairment, not a pullback. Drivers — funded_accounts: flat to slightly down; arpu: down ~25-35%; crypto_mix: collapses; nii_path: holds but cannot offset; multiple: ~10-12x.

- Retail Engagement Drop (15%, $61). Markets stay calm with low volatility; retail trading frequency fades without a crypto crash. Transaction revenue softens on lower volume even as funded accounts hold roughly flat; ARPU drifts lower. NII and Other (Gold/cards) provide ballast, so the de-rate is milder than a structural bust. Drivers — funded_accounts: flat; arpu: down ~10-15%; crypto_mix: lower; nii_path: stable; multiple: ~16x.

- Base (32%, $82). Funded accounts grow steadily and ARPU rises on deeper product attach (options, Gold, retirement); crypto mix normalizes to a mid-cycle level rather than boom or bust. NII holds with balances offsetting a modest rate-cut path, and Other scales as the fastest line. The multiple holds in the low-20s on proven diversification beyond pure transaction beta. Drivers — funded_accounts: up ~8-10%; arpu: up ~10%; crypto_mix: mid-cycle; nii_path: stable; multiple: ~22x.

- ME Bull (23%, $106). A strong risk-on tape lifts both crypto and options volume, driving an upside ARPU surprise on the existing funded base; NII stays elevated as margin balances and rates cooperate. Operating leverage expands margins as the asset-light model scales. The multiple expands as the market extrapolates the growth tape. Drivers — funded_accounts: up ~12%; arpu: up ~20-25%; crypto_mix: elevated; nii_path: elevated; multiple: ~28x.

- Product Expansion Win (10%, $146). The newer pillars inflect — Gold subscriptions, cards/spending, retirement AUC and advisory scale into a durable, less-cyclical revenue base that re-rates the mix away from transaction beta. Cortex AI and platform breadth lift engagement and ARPU structurally rather than cyclically. The market pays a higher multiple for the lower-beta, recurring-revenue trajectory and a larger AUC-driven NII base. Drivers — funded_accounts: up ~10-12%; arpu: up ~15-20% (recurring-led); crypto_mix: less dominant; nii_path: rising on AUC growth; multiple: ~30x.

Valuation Triangulation

Five anchors — but read them with their basis in mind. The Monte Carlo, the DCF terminal, and the peer re-rate all key off a market multiple, so they are not fully independent; only the discounted cash flows themselves are genuinely multiple-free. The discipline is to read the spread and weight the cash-based view, not to treat five numbers as five independent votes.

| Method | Basis | Fair Value | vs Spot |

|---|---|---|---|

| Monte Carlo median (Student-t + regime) | multiple | $54 | -52% |

| Sum-of-Parts | multiple | $76 | -32% |

| Peer P/E re-rate | multiple | $50 | -56% |

| Peer EV/Revenue re-rate | multiple | $49 | -57% |

| Scenario PWEV | multiple | $79 | -30% |

| DCF (5-year + terminal) | cash flow + terminal × | $65 | -42% |

| Triangulated (weighted) | — | $67 | -40% |

Peer EV/Revenue re-rate — 0% weight: it duplicates the peer-multiple information already carried by the Peer P/E anchor while ignoring margin mix; weighting both would double-count the peer view. Shown as a cross-check.

Monte Carlo — the distribution, not a point

10,000 paths, Student-t shocks (fat tails) with a regime-switching overlay. The median lands at $54 and 7% of paths finish above spot. The variance decomposition shows the p/e multiple is the dominant swing factor (84% of variance). Value is a multiple bet: fundamentals move the answer far less than the rating does.

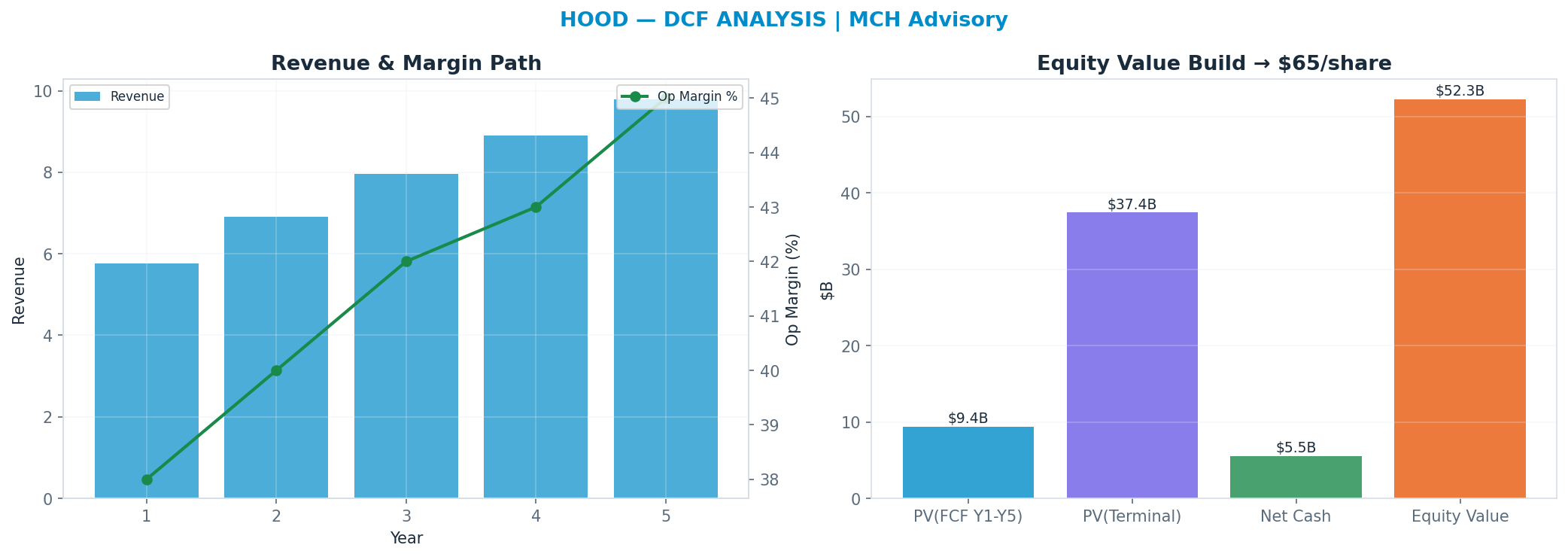

DCF — the cash-flow anchor

Independent of the market multiple: a 5-year path, WACC 11.0%, 18x terminal FCF multiple → $65. This anchor is deliberately the heaviest (35%): it is the valuation least hostage to the current multiple regime.

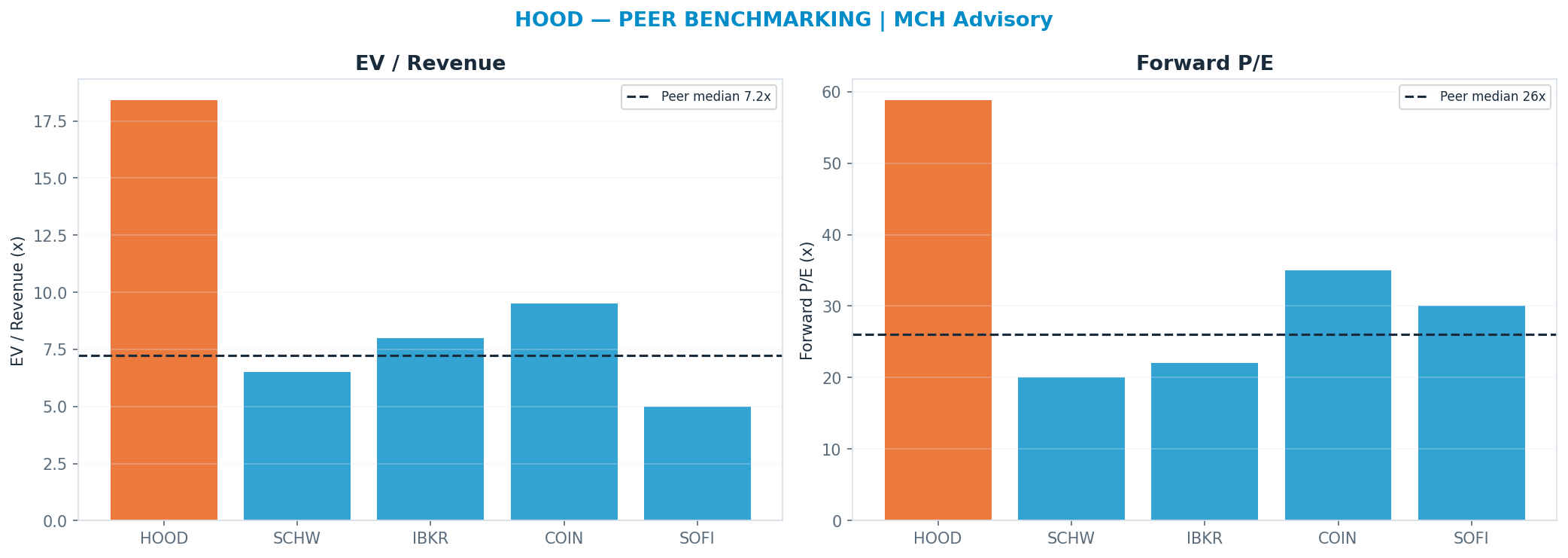

Peer benchmarking — relative value

Against the peer cohort, re-rating to the peer-median forward multiple (P/E 26.0x) implies $50. A premium is only justified by superior growth/margins; otherwise it is multiple risk. Weighted just 10% so the market's mood does not drive the fair value.

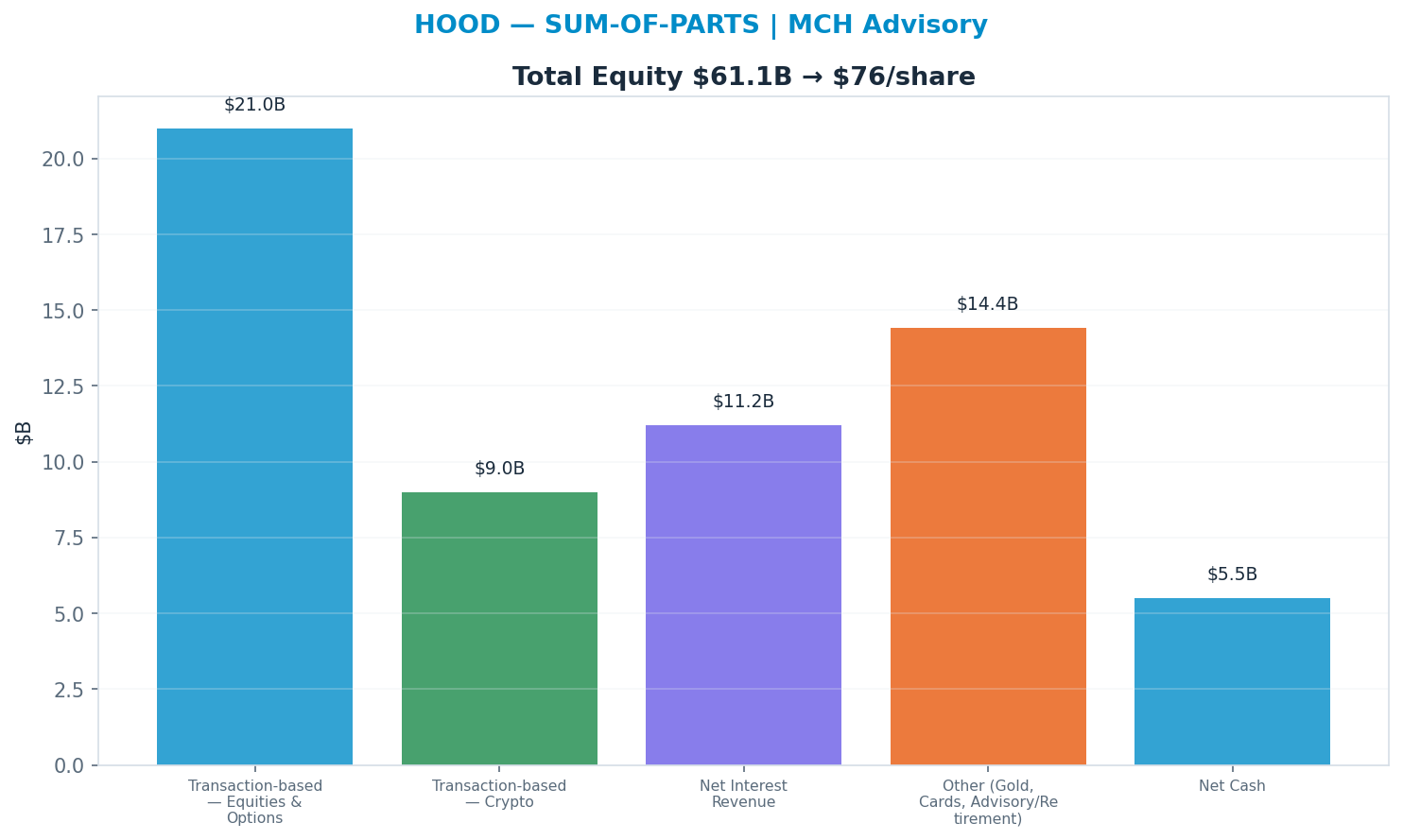

Sum-of-parts

Valuing each piece at the multiple it deserves (Transaction-based — Equities & Options 14x, Transaction-based — Crypto 10x, Net Interest Revenue 8x, Other (Gold, Cards, Advisory/Retirement) 18x) → $76. 'Transaction-based — Equities & Options' dominates at 14× → $21B (38% of EV) — the segment whose multiple matters most.

Across all anchors the spread is 47% of the median — wide (genuine disagreement — the blend carries low valuation confidence).

Revenue-Segment Breakdown

The company-specific drivers behind the valuation — each segment carries its own growth, margin, multiple and capex intensity. (Tags: FACT reported · ESTIMATE from disclosures · INFERENCE judgment.)

| Segment | Revenue | Mix | Growth | Op margin | EBIT | Multiple | Capex % | Tag |

|---|---|---|---|---|---|---|---|---|

| Transaction-based — Equities & Options | $1.5B | 33% | 20% | 55% | $0.8B | 14x | 1% | FACT/ESTIMATE |

| Transaction-based — Crypto | $0.9B | 20% | 25% | 50% | $0.5B | 10x | 1% | FACT/ESTIMATE |

| Net Interest Revenue | $1.4B | 30% | 10% | 65% | $0.9B | 8x | 0% | FACT/ESTIMATE |

| Other (Gold, Cards, Advisory/Retirement) | $0.8B | 17% | 30% | 45% | $0.4B | 18x | 2% | FACT/ESTIMATE |

| EBIT = segment revenue × operating margin (segment EBITDA not shown — per-segment D&A is not separately disclosed). |

Named Exposures

Crypto & market cyclicality (FACT/INFERENCE)

| Dimension | Assessment |

|---|---|

| Crypto share of transaction revenue | ~30-40% of transaction-based revenue and ~20% of total revenue (est.); swings sharply quarter-to-quarter with retail crypto activity |

| Engagement dependence | Revenue is geared to retail trading volume, which rises with volatility/speculation and falls in quiet tapes — high operating sensitivity to sentiment |

| Boom-bust history | 2021 retail/crypto boom inflated revenue; 2022 bust cut transaction revenue >50% YoY and drove a multi-quarter drawdown — a demonstrated structural-cyclicality risk, not hypothetical |

| Concentration | Transaction-based lines together are ~50-55% of revenue and are the most cyclical; a crypto winter compresses both volume and take-rate simultaneously |

| Tail risk | A crypto bear market plus a flat-vol equity tape can hit two transaction lines at once — correlated, not diversifying |

Rate sensitivity & regulation (ESTIMATE/INFERENCE)

| Dimension | Assessment |

|---|---|

| NII rate sensitivity | Net interest revenue (~30% of total) is rate-sensitive; a return toward zero-rate conditions could cut NII materially (est. order of magnitude: a sustained ~200bp cut pressures NII by a high-single to low-double-digit percent, balance-dependent) |

| Balance sensitivity | NII also scales with margin balances, cash-sweep deposits and securities-lending — outflows in a risk-off shock compress the base independently of rates |

| PFOF regulatory risk | Payment-for-order-flow underpins equities/options transaction revenue; an SEC ban or restriction (periodically debated) is a direct structural threat to the largest transaction line |

| Crypto regulatory risk | Token-listing scope, custody, staking and exchange registration remain contested; adverse rulings could force delistings or raise compliance cost on the crypto line |

| Mitigants | Diversification into Gold subscriptions, cards, retirement and advisory reduces single-line dependence over time, but does not offset a simultaneous rate-cut + PFOF-restriction shock |

Industry Context — Consumer Platforms

This name sits in the Consumer Platforms as a retail brokerage / fintech platform (equities, options, crypto). Net interest income on customer cash makes HOOD directly rate-sensitive; but the dominant swing factor is the crypto cycle and retail trading engagement, plus PFOF/crypto regulatory risk. Its scenarios are not guessed in isolation — they inherit a single, shared view of the cluster's driver cycle, so the names that depend on the same event are mutually consistent.

Value chain: UBER (mobility/delivery platform (Rides + Eats + Freight)) · HOOD (retail brokerage / fintech platform (equities, options, crypto))

| Shared state | Capex path | House view | This name implies |

|---|---|---|---|

| Consumer Recession / Regulatory | consumer pulls back + rate cuts hit NII; adverse regulatory rulings (gig reclassify / crypto crackdown) | 22% | 20% |

| Soft Patch / Disruption | sluggish consumer + the name-specific disruption tail bites (AV share for UBER, retail engagement fade for HOOD) | 18% | 15% |

| Base | steady consumer, rates drift, regulation manageable | 35% | 32% |

| Consumer Strength / Re-rate | strong consumer + risk-on tape; AV becomes a partner tailwind, crypto/product expansion inflects | 25% | 33% |

Mapping note: name-level 'ME Bull' (23%) + 'Product Expansion Win' (10%) map to cluster Consumer Strength / Re-rate (33%) — the cluster row is the SUM of the mapped scenario probabilities, not a different estimate.

On the cluster's key downside — Consumer Recession / Regulatory (consumer pulls back + rate cuts hit NII; adverse regulatory rulings (gig reclassify / crypto crackdown)) — this name implies 20% vs the cluster house view of 22% (in line with the house). The cluster's full cross-stock reconciliation governs that the names which ride the same capex cycle assign it comparable odds.

Structure: Consumer Demand — Both depend on discretionary consumer activity — UBER on ride/delivery frequency, HOOD on retail trading engagement. Soft consumer confidence pressures both, but via different mechanisms. (INFERENCE) Rate Sensitivity — HOOD is directly rate-sensitive via net interest income on customer cash/margin balances; UBER is indirectly rate-sensitive through consumer spending power and (more importantly) the discount rate applied to a long-duration growth/AV-optionality valuation. (FACT) Regulation — UBER faces gig-worker classification risk (driver reclassification raises cost structure); HOOD faces payment-for-order-flow (PFOF) scrutiny and crypto/securities regulatory overhang. Shared theme: both are regulated consumer-facing platforms exposed to policy shifts. (FACT) Disruption Tails — UBER's tail is robotaxi/AV (Waymo/Tesla) — a partner-and-supply upside or a network-displacement downside. HOOD's tail is the crypto cycle — a structural bust that removes a high-margin revenue and engagement pillar. These tails are uncorrelated with each other. (INFERENCE)

Model Appendix

DCF — line items

| Year | Revenue | Op income | − Capex | + D&A | FCF | PV(FCF) |

|---|---|---|---|---|---|---|

| FY+1 | $6B | $2B | $0B | $0B | $2B | $2B |

| FY+2 | $7B | $3B | $0B | $0B | $2B | $2B |

| FY+3 | $8B | $3B | $0B | $0B | $3B | $2B |

| FY+4 | $9B | $4B | $0B | $0B | $3B | $2B |

| FY+5 | $10B | $4B | $0B | $0B | $4B | $2B |

| Terminal | — | — | — | — | $4B × 18x | $37B |

FCF is bridged: NOPAT + D&A − Capex − ΔNWC (capex intensity 1% of revenue, weighted from the segments) — not a single conversion fudge.

WACC 11.0% · Σ PV(FCF) $9B + PV(terminal) $37B = EV $47B; + net cash → equity $52B ÷ diluted shares 0.80B = $65/share (exit-multiple terminal).

- Gordon (perpetuity-growth) terminal at 2.5% → $50/share — a genuinely non-multiple, cash-based cross-check; the exit-multiple and Gordon values bracket the terminal-value risk.

- Incremental ROIC on the forecast capex ≈ 444% vs WACC 11% → above WACC — the build is value-creative.

Peer set

| Peer | EV/Rev | Fwd P/E | Growth | Op margin |

|---|---|---|---|---|

| SCHW | 6.5x | 20x | 8% | 43% |

| IBKR | 8.0x | 22x | 15% | 70% |

| COIN | 9.5x | 35x | 25% | 38% |

| SOFI | 5.0x | 30x | 20% | 15% |

| Median | 7.25x | 26.0x | — | — |

Peer-median fwd P/E → $50; EV/Rev → $49.

Weighted fair-value math

| Anchor | Value | Weight | Contribution |

|---|---|---|---|

| DCF | $65 | 35% | $23 |

| Scenario PWEV | $79 | 25% | $20 |

| Monte Carlo median | $54 | 15% | $8 |

| Sum-of-parts | $76 | 15% | $11 |

| Peer P/E | $50 | 10% | $5 |

| Triangulated | — | 100% | $67 |

Sensitivity

DCF/share — WACC × terminal multiple

| WACC \ Term× | 12.6x | 15.3x | 18.0x | 20.7x | 23.4x |

|---|---|---|---|---|---|

| 9% | $55 | $63 | $71 | $78 | $86 |

| 10% | $53 | $61 | $68 | $75 | $83 |

| 11% | $51 | $58 | $65 | $72 | $79 |

| 12% | $50 | $56 | $63 | $70 | $76 |

| 13% | $48 | $54 | $61 | $67 | $74 |

DCF/share — revenue CAGR Δ × op-margin Δ

| CAGRΔ \ MgnΔ | -3.0pp | -1.5pp | +0.0pp | +1.5pp | +3.0pp |

|---|---|---|---|---|---|

| -3.0pp | $55 | $57 | $59 | $61 | $62 |

| -1.5pp | $58 | $60 | $62 | $64 | $66 |

| +0.0pp | $61 | $63 | $65 | $67 | $69 |

| +1.5pp | $65 | $67 | $69 | $71 | $73 |

| +3.0pp | $68 | $71 | $73 | $75 | $77 |

Tornado — DCF/share swing by driver (widest first)

| Driver | Low | High | Swing |

|---|---|---|---|

| Terminal × ±15% | $58 | $72 | $14 |

| Revenue CAGR ±3pp | $59 | $73 | $14 |

| Op margin ±3pp | $61 | $69 | $8 |

| WACC ±1pp | $63 | $68 | $5 |

| Capex intensity ±15% | $65 | $66 | $1 |

Company lever — SoP/share vs Other (Gold, Cards, Advisory/Retirement) multiple (AI re-rating) (base 18x)

| Multiple | 12.6x | 15.3x | 18.0x | 20.7x | 23.4x |

|---|---|---|---|---|---|

| SoP/share | $72 | $75 | $77 | $80 | $83 |

Consensus & Market Expectations

| Reference | Value |

|---|---|

| Street target (mean) | $105 (-7% vs spot · street) |

| House target | $79 (-25.1% vs street) |

| Sell-side coverage | 27 analysts (SB 4 / B 17 / H 4 / S 2 / SS 0; net score 0.43) |

| Consensus FY EPS | $2.58; house below (-25.5%) |

| Consensus FY revenue | $6.2B; house below (-13.1%) |

_Consensus figures: Alpha Vantage sell-side aggregates. Where the house view sits materially above or below the street, the divergence is itself a datum — see the thesis.

Balance Sheet & Liquidity

| Metric | Value |

|---|---|

| Net debt | $5.0B — highly levered |

| Net debt / EBITDA | 35.89x |

| Current ratio | 1.26x |

| Cash & ST investments | $10.5B |

Balance-sheet data as of 2025-12-31 (Alpha Vantage).

Capital Allocation

| Metric | Value |

|---|---|

| Free cash flow | $1.6B |

| Buybacks / dividends | $0.7B / $0.0B |

| Total shareholder yield | 0.7% |

| Payout as % of FCF | 41.2% |

| Reinvestment (capex / OCF) | 3.3% |

| SBC as % of FCF | 19.3% |

| Allocation stance | balanced |

Free-Cash-Flow Quality

| Metric | Value |

|---|---|

| FCF margin | 34.4% |

| FCF conversion (FCF / net income) | 84.1% |

| FCF yield | 1.8% |

| Capex intensity (capex / revenue) | 1.2% |

| FCF − SBC (diagnostic) | $1.3B |

| Capex split (maint / growth) | 55% / 45% — capex is tiny (~1% of revenue) for a software-driven broker; spend splits between maintaining platform/security/compliance infrastructure and growth investment in new-product engineering and international expansion. Economic investment is opex (headcount/marketing), not capitalised. |

Accounting quality: SBC 6.6% of revenue; cash conversion (OCF/NI) 87% — cash-backed.

Catalyst Calendar

- 2026-07-29 (~21d) — Quarterly earnings — est. EPS $0.41 (AV EARNINGS_CALENDAR)

- 2026-09-18 (~72d) — FOMC rate decision (authored)

- 2026-11-10 (~125d) — SEC rulemaking on payment-for-order-flow / order-execution (Reg NMS follow-through) (authored)

- 2027-02-20 (~227d) — Product-expansion milestone (retirement/advisory/international rollout) update (authored)

Forecast Track Record

- EPS surprise: beat 75.0% of the last 8 quarters; average surprise +24.0%.

- Prior-forecast backtest (7 snapshots, 2026-04-24→2026-07-06): directional hit-rate 0.0%; mean predicted -19.2% vs realized +40.3%. Disconfirming track record is reported, not suppressed.

Competitive Moat

Narrow moat. Robinhood's edge is a low-cost, mobile-native brand and a growing funded-account base with rising ARPU (crypto, options, cards, retirement, and PFOF-driven equities), but customers face low switching costs and the model is heavily geared to volatile retail activity and rate-sensitive net interest. That narrow moat cannot durably support a ~52x forward multiple; if engagement normalises and crypto/PFOF revenue proves cyclical rather than structural, the multiple should compress toward the 20-25x financial-platform range.

Moat sources:

- Low-cost, mobile-first brand with a large, still-growing young funded-account base

- Product-expansion flywheel (options, crypto, cards, retirement, advisory) lifting ARPU and net-deposit stickiness

- Net-interest revenue on customer cash/margin balances (rate-sensitive, not durable)

- NO strong moat vs switching costs, PFOF-regulation risk, and dependence on volatile retail engagement

Regulatory & Legal Risk

| Issue | Probability | Valuation sensitivity | Horizon |

|---|---|---|---|

| SEC restriction or ban on payment-for-order-flow (PFOF) and best-execution/order-routing rules | medium (~40%) | high - PFOF underpins a large share of transaction revenue; a ban is ~8-12% of FV | 12-24m |

| Crypto regulation/enforcement (token classification as securities, state licensing) affecting the crypto revenue line | high (~55%) | high - crypto is ~20% of total revenue; adverse rules are ~5-10% of FV | 12-24m |

| FINRA/state gamification, options-suitability and margin/PDT rule scrutiny raising compliance and lowering engagement | medium (~35%) | medium - ~2-4% of FV via engagement/ARPU drag | 12-24m |

Probabilities and sensitivities are analyst estimates, not market-implied.

Scenario Macro & Key Risks

| Scenario | Macro assumption | Key risk |

|---|---|---|

| Crypto Bust (Structural) | A sustained crypto bear market and adverse token regulation structurally shrink retail crypto trading. | Crypto transaction revenue (~20% of total) collapses and does not recover, resetting the growth algorithm. |

| Retail Engagement Drop | A quiet, low-volatility tape and waning retail speculation cut trading volumes across equities/options. | Engagement-driven transaction revenue falls faster than new-product ARPU can offset. |

| Base | Steady funded-account growth and ARPU expansion with rates gradually easing; crypto contributes but normalises. | Net-interest revenue erodes on rate cuts before new-product ARPU fully compensates. |

| ME Bull | Higher volatility/volumes and a firm rate environment lift both transaction and net-interest revenue. | The revenue surge is cyclical and reverses when volatility and rates fade. |

| Product Expansion Win | Retirement, advisory, cards and international scale materially, diversifying revenue away from crypto/PFOF. | New products underperform on adoption or margin, leaving the model still geared to volatile trading. |

What the Market Is Pricing In

At the current price, the market pays 43.8× forward EPS, vs the house DCF terminal 18.0×, and a peer median 26.0×. The house DCF sits 42% below spot, so the market is pricing in more than the house case — roughly 5.9pp of revenue CAGR.

Variant perception: the house view is below-consensus, and the thesis is primarily FCF-driven.

| Metric | Consensus | House | Importance |

|---|---|---|---|

| Revenue | 6.2 | 5.4 | High |

| EPS | 2.6 | 1.9 | Medium |

| Target price | 105.5 | 79.0 | Medium |

Peer Quality & Weighting

| Peer | Fwd P/E | Growth | Op margin | Quality | Weight cap |

|---|---|---|---|---|---|

| SCHW | 20.0× | 8% | 43% | broad | 25% |

| IBKR | 22.0× | 15% | 70% | broad | 25% |

| COIN | 35.0× | 25% | 38% | segment | 50% |

| SOFI | 30.0× | 20% | 15% | segment | 50% |

Quality-weighted forward P/E: 28.7× (simple median 26.0×). Direct peers count 100%, segment 50%, broad 25%.

Historical-range cross-check: 52-week range $64–$154, centre $99 (-12% vs spot); spot sits at the 55th percentile of the range. Low-weight mean-reversion cross-check, not a fundamental anchor.

Risk / Reward & Margin of Safety

| Metric | Value |

|---|---|

| Upside to triangulated FV | $67 (-40% vs spot · triangulated FV) |

| Downside to bear case (Crypto Bust (Structural)) | $37 (-67% vs spot · bear scenario) |

| Reward/risk ratio | 0.6× |

| Margin of safety (FV vs spot) | -68% |

| P(price > spot) — Monte Carlo | 7% |

Reward/risk compares triangulated upside against the probability-weighted bear target, not the extreme tail. Bull case (Product Expansion Win): $146.

Assumption Register

| Assumption | Value | Used in | Source |

|---|---|---|---|

| WACC | 11.0% | DCF discount rate | estimate (CAPM) |

| Terminal multiple | 18× | DCF exit value | estimate (peer-anchored) |

| Terminal growth | 2.5% | DCF Gordon terminal | estimate |

| SBC dilution | 3.0%/yr | PWEV, MC, DCF (charged once) | estimate (from SBC/rev) |

| EPS basis | consensus forward EPS (broker-adjusted, non-GAAP) | all forward P/E & scenario multiples | definition |

Sensitivity-ranked drivers (widest fair-value swing first): Terminal × ±15% (14.0); Revenue CAGR ±3pp (14.0); Op margin ±3pp (8.0); WACC ±1pp (5.0); Capex intensity ±15% (1.0).

Inputs, Sources & Confidence

Every load-bearing input, labelled by type and confidence. (reported fact · company guidance · consensus estimate · market data · house estimate · inference.)

| Input | Value | Type | Source | Confidence | Used in |

|---|---|---|---|---|---|

| Revenue TTM | $4.6B | reported fact | 10-K/10-Q via AV | High | Forecast base, EV/Rev |

| FY+1 guided revenue | $5.4B | company guidance | Company guidance | Medium | Forecast, SoP |

| Consensus FY EPS | $2.576 | consensus estimate | Sell-side consensus via AV | Medium | Variant perception |

| Diluted shares | 0.799B | reported fact | 10-K via AV | High | Market cap, per-share |

| Net debt / cash | $4.957B | reported fact | Balance sheet via AV | High | EV, DCF equity bridge |

| WACC | 11.0% | house estimate | CAPM (beta/rf) | Medium | DCF discount rate |

| Terminal multiple | 18× | house estimate | Peer/historical range | Medium | DCF exit value |

| Terminal growth | 2.5% | house estimate | Long-run GDP+ | Medium | DCF Gordon terminal |

| SBC dilution | 3.0%/yr | house estimate | From SBC/revenue | Medium | PWEV, MC, DCF (charged once) |

Source Log

| Source | Type | Date | Used for | Reference |

|---|---|---|---|---|

| Alpha Vantage — GLOBAL_QUOTE / OVERVIEW | market data | 2026-07-08 | Price, market cap, EV, 52-week range, forward P/E | mch_weekly_run live prices |

| Company income statement (10-K / 10-Q) via Alpha Vantage | reported fact | 2026-07-08 | Revenue, gross/operating margin, EBIT, interest expense | INCOME_STATEMENT / latest annual |

| Company balance sheet (10-K / 10-Q) via Alpha Vantage | reported fact | 2026-07-08 | Cash, debt, net debt, leases, equity, coverage | BALANCE_SHEET / latest annual |

| Company cash-flow statement (10-K / 10-Q) via Alpha Vantage | reported fact | 2026-07-08 | Operating cash flow, capex, FCF, buybacks, dividends, SBC | CASH_FLOW / latest annual |

| Company earnings releases via Alpha Vantage | reported fact | 2026-07-08 | Reported EPS, surprise history | EARNINGS / quarterly |

| Sell-side consensus via Alpha Vantage | consensus estimate | 2026-07-08 | Forward revenue/EPS consensus, analyst count | EARNINGS_ESTIMATES |

| Earnings calendar via Alpha Vantage | market data | 2026-07-08 | Next earnings date, catalyst timing | EARNINGS_CALENDAR |

| Company guidance | company guidance | 2026-07-08 | FY guided revenue / non-GAAP EPS basis | company guidance / earnings call |

| MCH segment model (from filings & disclosures) | house estimate | 2026-07-08 | Segment revenue, margins, multiples, AI decomposition | company_context (authored, tagged) |

| MCH qualitative analysis | inference | 2026-07-08 | Moat, regulatory risk, scenario macro, catalysts | company_context enrichment (authored) |

| MCH investment thesis & falsification triggers | house estimate | 2026-07-08 | Thesis, anti-thesis, thesis-break signals | authored §5.3 |

Citation coverage: 13/14 mandated claims sourced. Filing URLs are not available via the market-data provider; company statements are cited as 10-K/10-Q via Alpha Vantage.

Load-Bearing Assumptions

DCF: WACC 11%, terminal multiple 18×, FY+5 revenue $10B. Triangulation leans 35% on DCF, 25% on PWEV.

Reasons the Thesis Could Fail (Falsifiable)

Pre-registered signals that would break the thesis — each polices a specific scenario boundary and is checked at every earnings update:

- Crypto transaction revenue, YoY < -30% (2 consecutive prints → Consumer Recession / Regulatory). Crypto is the highest-beta transaction line; a sustained -30%+ contraction marks the Crypto Bust mechanism engaging rather than a single volatile quarter, midpoint between Base growth and the structural-bust collapse.

- Blended ARPU per funded account, YoY < -15% (2 consecutive prints → Soft Patch / Disruption). ARPU compression is the observable tell that engagement is fading; -15% sits between the Base ARPU rise and the Retail Engagement Drop decline, and two prints separate structural fade from noise.

- Net funded-account adds, QoQ < 0 (net outflow) (2 consecutive prints → Soft Patch / Disruption). The Base case rests on steady funded-account growth; two consecutive quarters of net account loss falsifies the compounding-user thesis and moves the name toward the engagement-drop path.

- Net interest revenue, YoY < -10% (2 consecutive prints → Consumer Recession / Regulatory). NII is the ballast in every bear scenario; a sustained double-digit decline signals rate cuts plus balance outflows hitting the cushion, removing the offset the Base case relies on.

- Adverse PFOF or crypto-listing ruling >= one binding regulatory action restricting PFOF economics or forcing token delistings (single event → Consumer Recession / Regulatory). A binding SEC PFOF restriction or crypto-listing crackdown is a discrete structural threat to the two largest transaction lines simultaneously; it validates the regulatory leg of the Crypto Bust scenario in a single event.

- Adjusted operating margin < 40% (2 consecutive prints → Soft Patch / Disruption). The asset-light thesis assumes operating leverage; margin slipping below 40% for two prints indicates cost growth outrunning revenue and undermines the EPS path across the Base and higher scenarios.

Fact / Inference / Speculation

- FACT: Spot $113; 52-week range $64–$154; engine rating SELL; base-case target $79 (-30%). (source: mch_weekly_run live prices, 8 July 2026)

- INFERENCE: Triangulated FV $67 (-40% vs spot · triangulated FV); the rating tracks the Monte-Carlo + scenario-PWEV core; the cash-flow anchor sits below the multiple-discipline core.

- SPECULATION: At current prices the embedded bet is that the market keeps paying the current multiple through the capex cycle — a regime call the engine cannot verify from fundamentals alone.

Recommendation: SELL

Defensive: rating SELL; triangulated fair value $67 (-40% vs spot) — the risk/reward is skewed to the downside on P/E Multiple. The debate is P/E Multiple — fundamentally a multiple/regime call. SBC runs $0.5bn TTM (~10% of revenue; charged once, as dilution).

Disclosures & Limitations

This report is for informational and research purposes only. It is not personalised investment advice and does not consider any investor's objectives, financial situation, risk tolerance, tax position, or liquidity needs.

- No suitability assessment has been performed for any individual.

- Market data may be delayed or inaccurate; figures are as of the analysis date.

- Model outputs (fair values, targets, scenario probabilities) are estimates and may be wrong.

- Forecasts are uncertain; past performance is not indicative of future returns.

- The author or publisher may hold positions in securities mentioned.

- Users should verify information against primary sources (company filings) before acting.

- Investing involves risk of loss; there is no guarantee any target price is achieved.

- Ratings follow a defined research methodology (12-month expected-return thresholds), not individual circumstances.