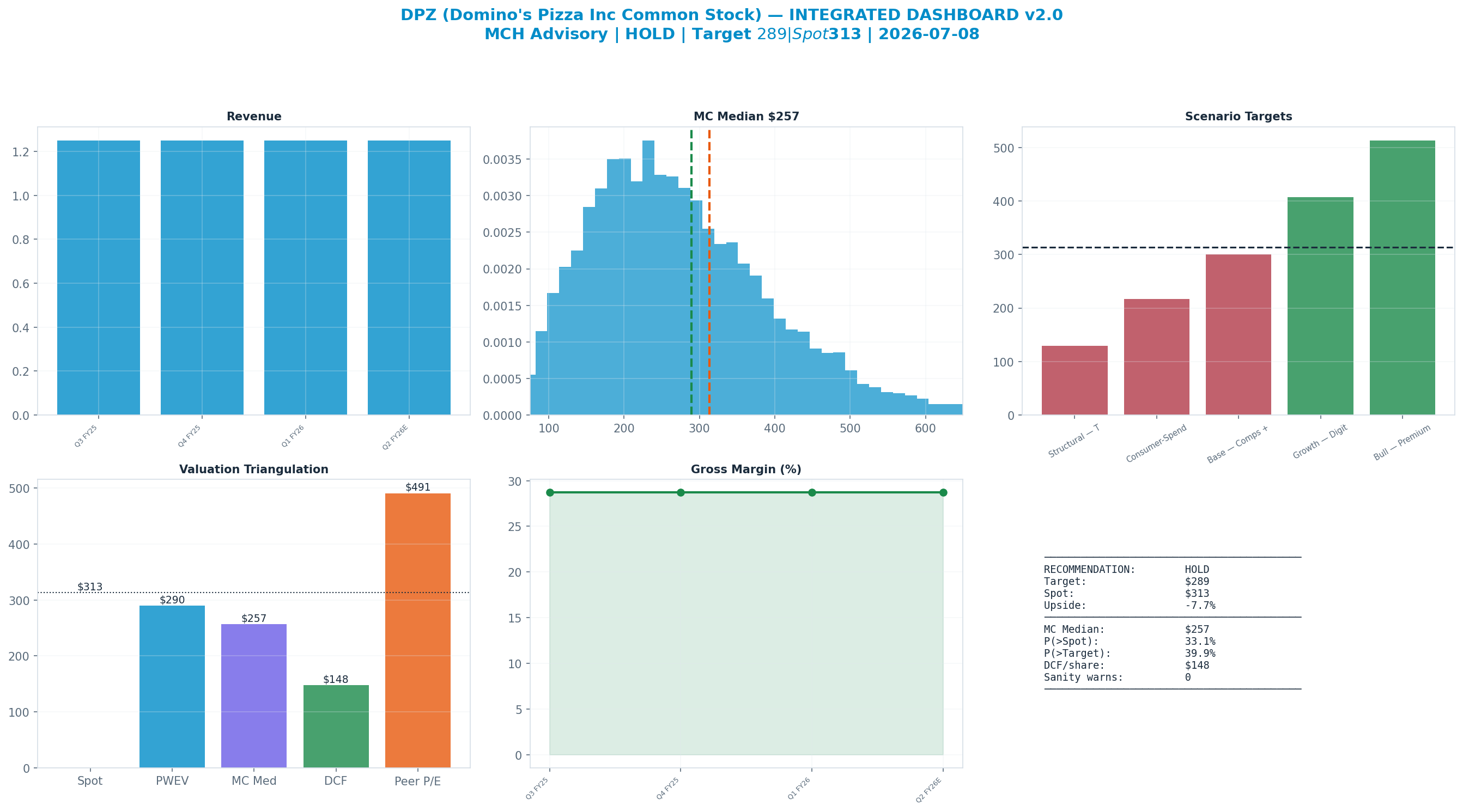

Rating: HOLD

HOLD (5-tier) · quality defensive · conviction: low

| Metric | Value |

|---|---|

| Current Price | $313 |

| Triangulated Fair Value | $217 (-31% vs spot · triangulated FV) |

| 12-mo Scenario PWEV | $290 (-7% vs spot · 12m PWEV) |

| Forward P/E | 16.3x |

| Market Cap | $10B |

| 52-Week Range | $282–$487 |

EPS basis for the forward P/E and all scenario multiples: consensus forward EPS (broker-adjusted, non-GAAP).

Methodology: Valuation triangulated across five independent anchors — Monte Carlo (Student-t + regime switching), an independent DCF, peer re-rating, a sum-of-parts, and a scenario-weighted PWEV. Figures reconciled to Alpha Vantage 2026-06-26. Each chart below sits with the part of the thesis it evidences.

General research for a skeptical institutional reader. Not personalised investment advice; no position sizing or trade instructions. Figures as of the analysis date; verify before acting.

Investment Committee Summary

| Rating | HOLD · HOLD (5-tier) |

| Classification · conviction | quality defensive · low |

| Triangulated fair value | $217 (-31% vs spot · triangulated FV) |

| 12-mo scenario PWEV | $290 (-7% vs spot · 12m PWEV) |

| Next catalyst | 2026-05-06 — Aggregator/third-party delivery (Uber Eats/DoorDash) contribution ramp update |

| Primary thesis-break | US same-store sales growth (comps) < 0.005 (2 consecutive prints) |

📎 Download the full model (Excel) — DCF line items, scenarios, sensitivity, assumptions, and extended fundamentals.

Rating Bridge

Rating = HOLD because:

- Probability-weighted scenario value implies -7% vs spot

- Monte Carlo median implies -18% vs spot

- DCF fair value implies -53% vs spot — but this is terminal-value sensitive (exit-multiple $148 vs Gordon $238, 62% apart), so it carries less weight

- Bear case (Structural — Traffic Loss / GLP-1 / Saturation) downside is -59% vs spot

- Net: reward/risk of 0.5× is not asymmetric enough for a Buy and not impaired enough for a Sell — hence Hold.

Investment Thesis

At $296 on roughly 33m diluted shares, spot capitalises about $20 of Base earnings at a mid-teens multiple — a market pricing Domino's as a mature, saturated US franchisor with limited comp runway and a live GLP-1 overhang. The engine's Base path recovers a similar $300 target from 5% growth and a 15.9% margin, but the probability-weighted target of $289 sits marginally below spot because the structural and recession scenarios together carry 37% weight and pull toward $127–$216. The rating is HOLD: the triangulated value clusters near price, and the standalone DCF anchors far lower at $146 (Gordon variant $236), so the market multiple, not cash flow, is doing the work. Value is triangulated across scenario paths, the capex-bridge DCF and a franchisor peer set trading richer on EV/revenue. The single most damaging risk is a durable step-down in US order frequency — if GLP-1 adoption structurally lowers pizza occasions, comps and the multiple compress together toward the sub-$130 structural case.

The dashboard below is the whole argument on one page: spot ($313) against each valuation anchor, the scenario tree, technicals and the options-implied move.

Anti-Thesis (The Real Bear Case)

The highest-probability bear is the structural traffic-loss case, weighted at 20%. Its mechanism is not a soft quarter but a permanent reset of US demand: GLP-1 adoption lowers order frequency, saturated trade areas cap net new units, and delivery aggregators erode the carry-out and app advantage that underpins the franchisee royalty stream. Once same-store sales turn negative, the securitised balance sheet works against the equity — fixed debt service consumes free cash, the buyback that flatters per-share growth is curtailed, and the multiple de-rates to a cyclical trough near 8x. Earnings and the multiple then fall in tandem, which is precisely why the structural target of $127 sits below the 52-week low of $282. In that world the mid-teens multiple was never a floor.

Key Debate

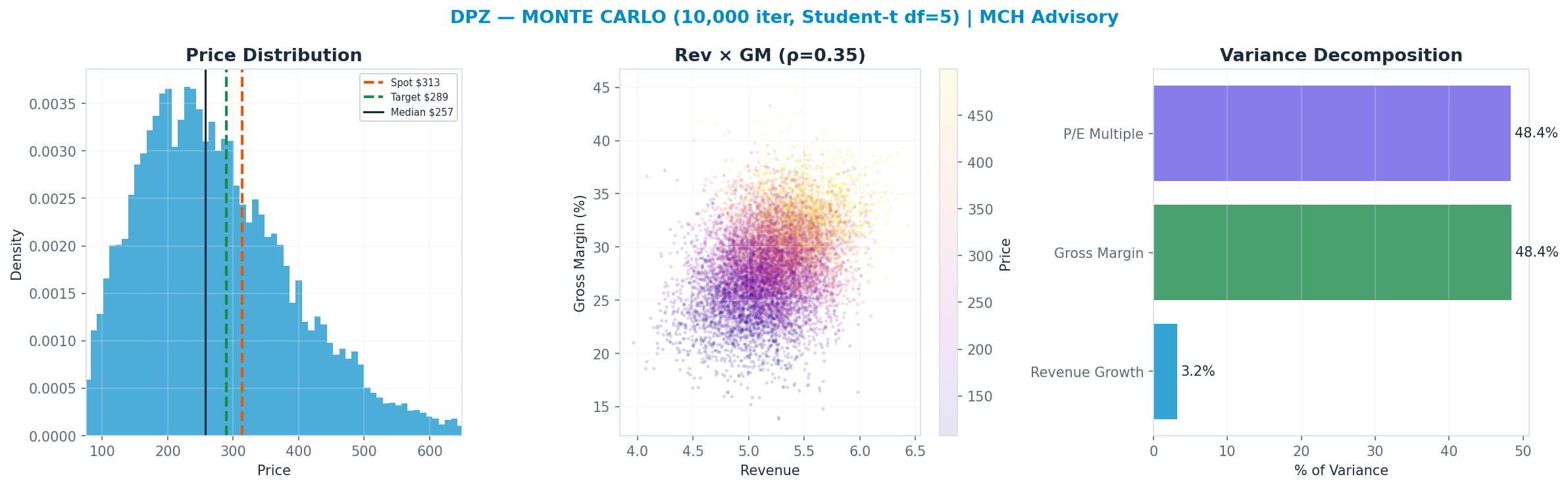

Gross Margin explains 48% of Monte Carlo outcome variance — the single variable that decides which side is right.

Earnings-Call Disconfirmation & Sentiment

Derived signals from the MCH market-data store (Alpha Vantage transcripts + news). Quantitative tone only — a disconfirmation flag, not a substitute for reading the call.

Management vs analyst tone (2026Q1): management +0.39 vs analyst floor +0.00 → delta +0.39 (n=36 mgmt / 18 Q&A; 50th pctile across the S&P book, z -0.0).

Flag: TYPICAL — management-vs-analyst tone within the normal cross-sectional range.

| Quarter | Mgmt | Analyst | Delta |

|---|---|---|---|

| 2026Q1 | +0.39 | +0.00 | +0.39 |

| 2025Q4 | +0.52 | +0.20 | +0.32 |

| 2025Q3 | +0.47 | +0.21 | +0.27 |

| 2025Q2 | +0.47 | +0.24 | +0.23 |

News (last 365d, 1000 articles): avg ticker sentiment +0.12 (bullish 15% / bearish 5%)

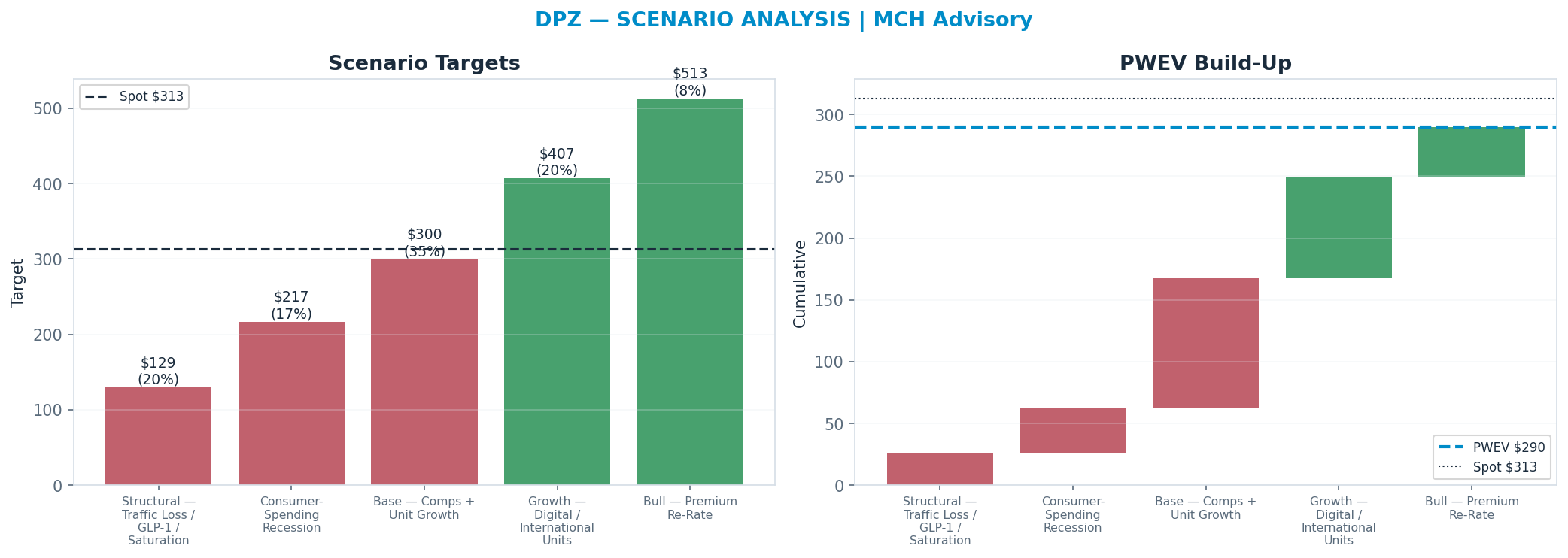

Scenario Analysis

The tree runs from a structural 'Structural — Traffic Loss / GLP-1 / Saturation' downside ($129) to a 'Bull — Premium Re-Rate' bull case ($513); the probability-weighted blend (PWEV $290) is -7% versus spot.

| Scenario | Probability | Target | Return vs spot |

|---|---|---|---|

| Structural — Traffic Loss / GLP-1 / Saturation | 20% | $129 | -59% |

| Consumer-Spending Recession | 17% | $217 | -31% |

| Base — Comps + Unit Growth | 35% | $300 | -4% |

| Growth — Digital / International Units | 20% | $407 | +30% |

| Bull — Premium Re-Rate | 8% | $513 | +64% |

| Probability-Weighted (PWEV) | — | $290 | -7% |

Scenario rationale — what each probability buys (the driver path behind every target):

- Structural — Traffic Loss / GLP-1 / Saturation (20%, $129). Structural impairment — traffic loss / GLP-1 / saturation: earnings AND the multiple compress together. Target sits below the 52-week low by construction. Drivers — implied_target: 127.18; probability: 0.2.

- Consumer-Spending Recession (17%, $217). Cyclical downturn — restaurant traffic + comps + unit growth vs labor/commodity costs (GLP-1 debate) weakens for 1–2 years before normalising. Drivers — implied_target: 215.98; probability: 0.17.

- Base — Comps + Unit Growth (35%, $300). Mid-cycle — normalised restaurant traffic + comps + unit growth vs labor/commodity costs (GLP-1 debate); disciplined capital allocation; steady returns. Drivers — implied_target: 299.97; probability: 0.35.

- Growth — Digital / International Units (20%, $407). Upside — digital + international unit growth lifts earnings above mid-cycle; the multiple expands modestly. Drivers — implied_target: 404.96; probability: 0.2.

- Bull — Premium Re-Rate (8%, $513). Upside tail — sustained tight conditions or a structural re-rate on digital + international unit growth. Drivers — implied_target: 511.45; probability: 0.08.

Valuation Triangulation

Five anchors — but read them with their basis in mind. The Monte Carlo, the DCF terminal, and the peer re-rate all key off a market multiple, so they are not fully independent; only the discounted cash flows themselves are genuinely multiple-free. The discipline is to read the spread and weight the cash-based view, not to treat five numbers as five independent votes.

| Method | Basis | Fair Value | vs Spot |

|---|---|---|---|

| Monte Carlo median (Student-t + regime) | multiple | $257 | -18% |

| Peer P/E re-rate | multiple | $491 | +57% |

| Peer EV/Revenue re-rate | multiple | $610 | +95% |

| Scenario PWEV | multiple | $290 | -7% |

| DCF (5-year + terminal) | cash flow + terminal × | $148 | -53% |

| Triangulated (weighted) | — | $217 | -31% |

Peer EV/Revenue re-rate — 0% weight: it duplicates the peer-multiple information already carried by the Peer P/E anchor while ignoring margin mix; weighting both would double-count the peer view. Shown as a cross-check.

peer P/E re-rate excluded from the weighted blend — diverges >55% from the Monte-Carlo / scenario core. For a high-leverage equity the per-share DCF (enterprise value less large net debt) is hypersensitive to the terminal multiple; a peer re-rate across heterogeneous margins is apples-to-oranges. Shown above for reference; the blend leans on the multiple-discipline and scenario anchors.

Rating vs blend — the key debate. The rating tracks the multiple-discipline fair value (Monte Carlo $257 + scenario PWEV $290, ≈ spot); the weighted blend $217 (-31%) sits below it because the cash-flow DCF ($148) is materially more conservative than the market multiple. Whether the current multiple is justified is the central question for this name — and the principal downside risk to the rating.

Monte Carlo — the distribution, not a point

10,000 paths, Student-t shocks (fat tails) with a regime-switching overlay. The median lands at $257 and 33% of paths finish above spot. The variance decomposition shows the gross margin is the dominant swing factor (48% of variance). The fundamental driver, not the multiple, sets the spread — a cleaner setup.

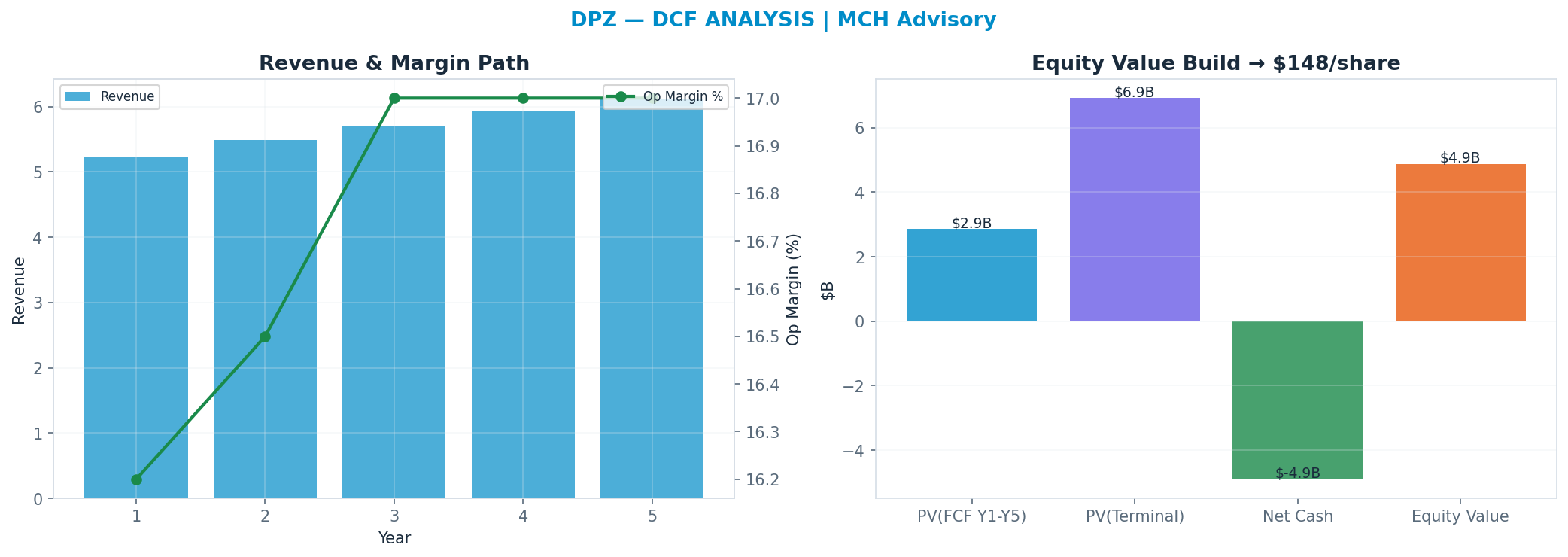

DCF — the cash-flow anchor

Independent of the market multiple: a 5-year path, WACC 8.0%, 13x terminal FCF multiple → $148. This anchor is deliberately the heaviest (41%): it is the valuation least hostage to the current multiple regime.

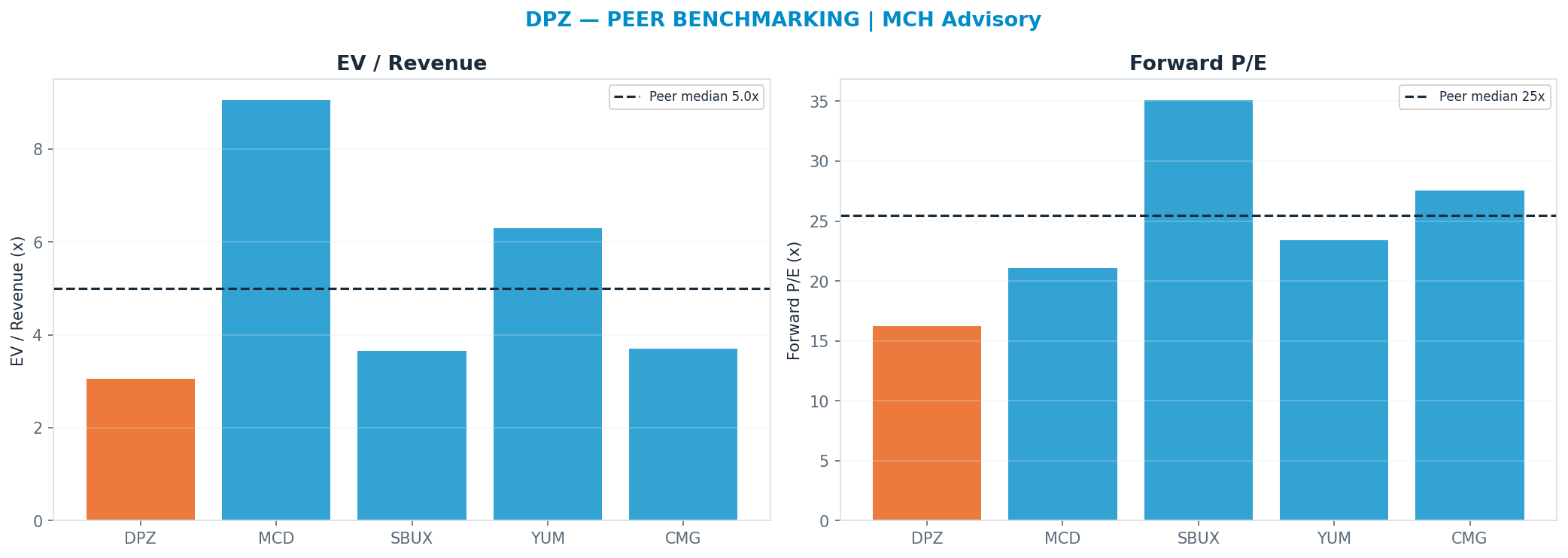

Peer benchmarking — relative value

Against the peer cohort, re-rating to the peer-median forward multiple (P/E 25.485x) implies $491. A premium is only justified by superior growth/margins; otherwise it is multiple risk. Weighted just 12% so the market's mood does not drive the fair value.

Across all anchors the spread is 159% of the median — wide (genuine disagreement — the blend carries low valuation confidence).

Revenue-Segment Breakdown

The company-specific drivers behind the valuation — each segment carries its own growth, margin, multiple and capex intensity. (Tags: FACT reported · ESTIMATE from disclosures · INFERENCE judgment.)

| Segment | Revenue | Mix | Growth | Op margin | EBIT | Multiple | Capex % | Tag |

|---|---|---|---|---|---|---|---|---|

| Restaurants (franchised / company) | $5.0B | 100% | 5% | 16% | $0.8B | 15x | 5% | ESTIMATE |

| EBIT = segment revenue × operating margin (segment EBITDA not shown — per-segment D&A is not separately disclosed). |

Named Exposures

Demand & pricing cycle (FACT/ESTIMATE)

| Dimension | Assessment |

|---|---|

| driver | restaurant traffic + comps + unit growth vs labor/commodity costs (GLP-1 debate) |

| net_debt_or_cash_b | -4.9 |

Capital intensity & shareholder returns (ESTIMATE)

| Dimension | Assessment |

|---|---|

| capex_pct_revenue | 0.05 |

| div_yield | 0.0251 |

Structural risk vs optionality (INFERENCE)

| Dimension | Assessment |

|---|---|

| downside | traffic loss / GLP-1 / saturation |

| upside | digital + international unit growth |

Industry Context — Consumer Discretionary — Restaurants

This name sits in the Consumer Discretionary — Restaurants as a restaurants. restaurant traffic + comps + unit growth vs labor/commodity costs (GLP-1 debate) Its scenarios are not guessed in isolation — they inherit a single, shared view of the cluster's driver cycle, so the names that depend on the same event are mutually consistent.

Value chain: MCD (restaurants) · SBUX (restaurants) · YUM (restaurants) · CMG (restaurants) · DRI (restaurants) · DPZ (restaurants)

| Shared state | Capex path | House view | This name implies |

|---|---|---|---|

| Traffic Recession — GLP-1 / Consumer Pullback | 37% | 37% | |

| Mid-Cycle — Comps + Unit Growth | 35% | 35% | |

| Upside — Digital / International Units | 28% | 28% |

Mapping note: name-level 'Structural — Traffic Loss / GLP-1 / Saturation' (20%) + 'Consumer-Spending Recession' (17%) map to cluster Traffic Recession — GLP-1 / Consumer Pullback (37%); name-level 'Growth — Digital / International Units' (20%) + 'Bull — Premium Re-Rate' (8%) map to cluster Upside — Digital / International Units (28%) — the cluster row is the SUM of the mapped scenario probabilities, not a different estimate.

On the cluster's key downside — Traffic Recession — GLP-1 / Consumer Pullback () — this name implies 37% vs the cluster house view of 37% (in line with the house). The cluster's full cross-stock reconciliation governs that the names which ride the same capex cycle assign it comparable odds.

Structure: Shared State — The disc_restaurants cycle is the shared macro driver. Driver — restaurant traffic + comps + unit growth vs labor/commodity costs Dispersion — Members differ by cyclicality (quality compounders vs deep cyclicals).

Model Appendix

DCF — line items

| Year | Revenue | Op income | − Capex | + D&A | FCF | PV(FCF) |

|---|---|---|---|---|---|---|

| FY+1 | $5B | $1B | $0B | $0B | $1B | $1B |

| FY+2 | $5B | $1B | $0B | $0B | $1B | $1B |

| FY+3 | $6B | $1B | $0B | $0B | $1B | $1B |

| FY+4 | $6B | $1B | $0B | $0B | $1B | $1B |

| FY+5 | $6B | $1B | $0B | $0B | $1B | $1B |

| Terminal | — | — | — | — | $1B × 13x | $7B |

FCF is bridged: NOPAT + D&A − Capex − ΔNWC (capex intensity 5% of revenue, weighted from the segments) — not a single conversion fudge.

WACC 8.0% · Σ PV(FCF) $3B + PV(terminal) $7B = EV $10B; + net cash → equity $5B ÷ diluted shares 0.03B = $148/share (exit-multiple terminal).

- Gordon (perpetuity-growth) terminal at 2.5% → $238/share — a genuinely non-multiple, cash-based cross-check; the exit-multiple and Gordon values bracket the terminal-value risk.

- Incremental ROIC on the forecast capex ≈ 20% vs WACC 8% → above WACC — the build is value-creative.

Peer set

| Peer | EV/Rev | Fwd P/E | Growth | Op margin |

|---|---|---|---|---|

| MCD | 9.05x | 21.1x | 5% | 44% |

| SBUX | 3.646x | 35.09x | 5% | 8% |

| YUM | 6.3x | 23.42x | 5% | 31% |

| CMG | 3.709x | 27.55x | 5% | 13% |

| Median | 5.0045x | 25.485x | — | — |

Peer-median fwd P/E → $491; EV/Rev → $610.

Weighted fair-value math

| Anchor | Value | Weight | Contribution |

|---|---|---|---|

| DCF | $148 | 47% | $69 |

| Scenario PWEV | $290 | 33% | $97 |

| Monte Carlo median | $257 | 20% | $51 |

| Triangulated | — | 100% | $217 |

Sensitivity

DCF/share — WACC × terminal multiple

| WACC \ Term× | 9.1x | 11.0x | 13.0x | 14.9x | 16.9x |

|---|---|---|---|---|---|

| 6% | $104 | $138 | $173 | $207 | $242 |

| 7% | $94 | $126 | $160 | $192 | $226 |

| 8% | $85 | $115 | $148 | $178 | $210 |

| 9% | $76 | $105 | $136 | $165 | $196 |

| 10% | $67 | $95 | $125 | $153 | $182 |

DCF/share — revenue CAGR Δ × op-margin Δ

| CAGRΔ \ MgnΔ | -3.0pp | -1.5pp | +0.0pp | +1.5pp | +3.0pp |

|---|---|---|---|---|---|

| -3.0pp | $64 | $88 | $111 | $135 | $159 |

| -1.5pp | $79 | $104 | $129 | $154 | $179 |

| +0.0pp | $94 | $121 | $148 | $174 | $201 |

| +1.5pp | $110 | $139 | $167 | $196 | $225 |

| +3.0pp | $127 | $158 | $188 | $219 | $249 |

Tornado — DCF/share swing by driver (widest first)

| Driver | Low | High | Swing |

|---|---|---|---|

| Op margin ±3pp | $94 | $201 | $107 |

| Revenue CAGR ±3pp | $111 | $188 | $77 |

| Terminal × ±15% | $116 | $179 | $63 |

| WACC ±1pp | $136 | $160 | $24 |

| Capex intensity ±15% | $139 | $157 | $18 |

Company lever — SoP/share vs Restaurants (franchised / company) multiple (AI re-rating) (base 15x)

| Multiple | 10.5x | 12.8x | 15.0x | 17.2x | 19.5x |

|---|---|---|---|---|---|

| SoP/share | $1,442 | $1,791 | $2,124 | $2,458 | $2,806 |

Consensus & Market Expectations

| Reference | Value |

|---|---|

| Street target (mean) | $400 (+28% vs spot · street) |

| House target | $289 (-27.8% vs street) |

| Sell-side coverage | 31 analysts (SB 2 / B 15 / H 12 / S 1 / SS 1; net score 0.26) |

| Consensus FY EPS | $20.97; house below (-8.1%) |

| Consensus FY revenue | $5.4B; house below (-3.5%) |

_Consensus figures: Alpha Vantage sell-side aggregates. Where the house view sits materially above or below the street, the divergence is itself a datum — see the thesis.

Balance Sheet & Liquidity

| Metric | Value |

|---|---|

| Net debt | $4.8B — highly levered |

| Net debt / EBITDA | 4.70x |

| Interest coverage (EBIT / interest) | 4.9x |

| Current ratio | 1.65x |

| Lease obligations | $0.2B |

| Cash & ST investments | $0.4B |

Balance-sheet data as of 2025-12-31 (Alpha Vantage).

Capital Allocation

| Metric | Value |

|---|---|

| Free cash flow | $0.7B |

| Buybacks / dividends | $0.4B / $0.2B |

| Total shareholder yield | 5.8% |

| Payout as % of FCF | 88.5% |

| Reinvestment (capex / OCF) | 15.3% |

| SBC as % of FCF | 6.7% |

| Allocation stance | returns-heavy |

Free-Cash-Flow Quality

| Metric | Value |

|---|---|

| FCF margin | 13.4% |

| FCF conversion (FCF / net income) | 111.6% |

| FCF yield | 6.5% |

| Capex intensity (capex / revenue) | 2.4% |

| FCF − SBC (diagnostic) | $0.6B |

| Capex split (maint / growth) | 55% / 45% — Asset-light franchisor; corporate capex is modest — maintenance covers existing supply-chain centres and technology, growth capex funds new commissary capacity and digital platform build |

Accounting quality: SBC 0.9% of revenue; cash conversion (OCF/NI) 132% — cash-backed.

Catalyst Calendar

- 2026-05-06 (~-63d) — Aggregator/third-party delivery (Uber Eats/DoorDash) contribution ramp update (authored)

- 2026-07-20 (~12d) — Quarterly earnings — est. EPS $4.15 (AV EARNINGS_CALENDAR)

- 2026-09-15 (~69d) — International net-unit-growth and master-franchisee health update (authored)

- 2027-02-24 (~231d) — FY2027 global-comp and unit-growth guidance (authored)

Forecast Track Record

- EPS surprise: beat 50.0% of the last 8 quarters; average surprise +3.3%.

Competitive Moat

Wide moat. An asset-light, high-return franchise model with the largest US pizza scale, proprietary digital ordering platform and supply-chain (dough/commissary) economics supports a terminal multiple above the market ~16x; falsifiable claim — if US same-store comps cannot sustain positive low-single-digit growth as the GLP-1 and saturation overhang bites, the growth moat is impaired and the mid-teens multiple should compress toward a mature-franchisor low-teens.

Moat sources:

- Largest US pizza scale with density-driven delivery economics and brand

- Proprietary digital ordering platform and loyalty data (majority of sales digital)

- Vertically integrated dough/commissary supply chain generating franchisee-tied margin

- Asset-light franchise model — high ROIC, royalty/supply-chain fee stream

Regulatory & Legal Risk

| Issue | Probability | Valuation sensitivity | Horizon |

|---|---|---|---|

| Minimum-wage / franchise-labour and joint-employer regulation raising franchisee cost and unit economics | medium (~45%) | medium - pressures franchisee returns and thus net unit growth ~4-6% of FV | 12-24m |

| Food-labelling / menu and delivery-fee regulation in key US/international markets | low (~25%) | low - modest compliance/pricing impact ~2% of FV | 12-24m |

Probabilities and sensitivities are analyst estimates, not market-implied.

Scenario Macro & Key Risks

| Scenario | Macro assumption | Key risk |

|---|---|---|

| Structural — Traffic Loss / GLP-1 / Saturation | GLP-1 appetite suppression, US market saturation and aggregator-driven competition structurally erode order frequency and net unit growth | US comps turn persistently negative — the growth-franchise premium collapses to a mature-franchisor multiple |

| Consumer-Spending Recession | Discretionary and QSR spending pullback pressures traffic and average ticket | Value-seeking trade-down helps traffic but compresses ticket and franchisee margins |

| Base — Comps + Unit Growth | Low-single-digit global comps, steady international net unit growth and stable US franchise economics | US comps stall while international carries the load, keeping the market from paying up |

| Growth — Digital / International Units | Digital/loyalty and aggregator channels lift order frequency while international units compound net growth | Aggregator economics dilute margin, and international unit growth depends on master-franchisee health |

| Bull — Premium Re-Rate | Sustained comps, accelerated units and digital margin gains restore a premium growth-franchisor multiple | The GLP-1/saturation overhang caps multiple expansion even if fundamentals hold |

What the Market Is Pricing In

At the current price, the market pays 14.9× forward EPS, vs the house DCF terminal 13.0×, and a peer median 25.485×. The house DCF sits 53% below spot, so the market is pricing in more than the house case — roughly 3.0pp of revenue CAGR.

Variant perception: the house view is below-consensus, and the thesis is primarily event-driven.

| Metric | Consensus | House | Importance |

|---|---|---|---|

| Revenue | 5.4 | 5.2 | High |

| EPS | 21.0 | 19.3 | Medium |

| Target price | 400.4 | 289.1 | Medium |

Peer Quality & Weighting

| Peer | Fwd P/E | Growth | Op margin | Quality | Weight cap |

|---|---|---|---|---|---|

| MCD | 21.1× | 5% | 44% | segment | 50% |

| SBUX | 35.09× | 5% | 8% | broad | 25% |

| YUM | 23.42× | 5% | 31% | segment | 50% |

| CMG | 27.55× | 5% | 13% | broad | 25% |

Quality-weighted forward P/E: 25.3× (simple median 25.485×). Direct peers count 100%, segment 50%, broad 25%.

Historical-range cross-check: 52-week range $282–$487, centre $370 (+18% vs spot); spot sits at the 15th percentile of the range. Low-weight mean-reversion cross-check, not a fundamental anchor.

Risk / Reward & Margin of Safety

| Metric | Value |

|---|---|

| Upside to triangulated FV | $217 (-31% vs spot · triangulated FV) |

| Downside to bear case (Structural — Traffic Loss / GLP-1 / Saturation) | $129 (-59% vs spot · bear scenario) |

| Reward/risk ratio | 0.5× |

| Margin of safety (FV vs spot) | -44% |

| P(price > spot) — Monte Carlo | 33% |

Reward/risk compares triangulated upside against the probability-weighted bear target, not the extreme tail. Bull case (Bull — Premium Re-Rate): $513.

Assumption Register

| Assumption | Value | Used in | Source |

|---|---|---|---|

| WACC | 8.0% | DCF discount rate | estimate (CAPM) |

| Terminal multiple | 13× | DCF exit value | estimate (peer-anchored) |

| Terminal growth | 2.5% | DCF Gordon terminal | estimate |

| SBC dilution | 0.0%/yr | PWEV, MC, DCF (charged once) | estimate (from SBC/rev) |

| EPS basis | consensus forward EPS (broker-adjusted, non-GAAP) | all forward P/E & scenario multiples | definition |

Sensitivity-ranked drivers (widest fair-value swing first): Op margin ±3pp (107.0); Revenue CAGR ±3pp (77.0); Terminal × ±15% (63.0); WACC ±1pp (24.0); Capex intensity ±15% (18.0).

Inputs, Sources & Confidence

Every load-bearing input, labelled by type and confidence. (reported fact · company guidance · consensus estimate · market data · house estimate · inference.)

| Input | Value | Type | Source | Confidence | Used in |

|---|---|---|---|---|---|

| Revenue TTM | $5.0B | reported fact | 10-K/10-Q via AV | High | Forecast base, EV/Rev |

| FY+1 guided revenue | $5.2B | company guidance | Company guidance | Medium | Forecast, SoP |

| Consensus FY EPS | $20.9655 | consensus estimate | Sell-side consensus via AV | Medium | Variant perception |

| Diluted shares | 0.033B | reported fact | 10-K via AV | High | Market cap, per-share |

| Net debt / cash | $4.798B | reported fact | Balance sheet via AV | High | EV, DCF equity bridge |

| WACC | 8.0% | house estimate | CAPM (beta/rf) | Medium | DCF discount rate |

| Terminal multiple | 13× | house estimate | Peer/historical range | Medium | DCF exit value |

| Terminal growth | 2.5% | house estimate | Long-run GDP+ | Medium | DCF Gordon terminal |

Source Log

| Source | Type | Date | Used for | Reference |

|---|---|---|---|---|

| Alpha Vantage — GLOBAL_QUOTE / OVERVIEW | market data | 2026-07-08 | Price, market cap, EV, 52-week range, forward P/E | Alpha Vantage 2026-06-26 |

| Company income statement (10-K / 10-Q) via Alpha Vantage | reported fact | 2026-07-08 | Revenue, gross/operating margin, EBIT, interest expense | INCOME_STATEMENT / latest annual |

| Company balance sheet (10-K / 10-Q) via Alpha Vantage | reported fact | 2026-07-08 | Cash, debt, net debt, leases, equity, coverage | BALANCE_SHEET / latest annual |

| Company cash-flow statement (10-K / 10-Q) via Alpha Vantage | reported fact | 2026-07-08 | Operating cash flow, capex, FCF, buybacks, dividends, SBC | CASH_FLOW / latest annual |

| Company earnings releases via Alpha Vantage | reported fact | 2026-07-08 | Reported EPS, surprise history | EARNINGS / quarterly |

| Sell-side consensus via Alpha Vantage | consensus estimate | 2026-07-08 | Forward revenue/EPS consensus, analyst count | EARNINGS_ESTIMATES |

| Earnings calendar via Alpha Vantage | market data | 2026-07-08 | Next earnings date, catalyst timing | EARNINGS_CALENDAR |

| Company guidance | company guidance | 2026-07-08 | FY guided revenue / non-GAAP EPS basis | company guidance / earnings call |

| MCH segment model (from filings & disclosures) | house estimate | 2026-07-08 | Segment revenue, margins, multiples, AI decomposition | company_context (authored, tagged) |

| MCH qualitative analysis | inference | 2026-07-08 | Moat, regulatory risk, scenario macro, catalysts | company_context enrichment (authored) |

| MCH investment thesis & falsification triggers | house estimate | 2026-07-08 | Thesis, anti-thesis, thesis-break signals | authored §5.3 |

Citation coverage: 13/14 mandated claims sourced. Filing URLs are not available via the market-data provider; company statements are cited as 10-K/10-Q via Alpha Vantage.

Load-Bearing Assumptions

DCF: WACC 8%, terminal multiple 13×, FY+5 revenue $6B. Triangulation leans 41% on DCF, 29% on PWEV.

Reasons the Thesis Could Fail (Falsifiable)

Pre-registered signals that would break the thesis — each polices a specific scenario boundary and is checked at every earnings update:

- US same-store sales growth (comps) < 0.005 (2 consecutive prints → Traffic Recession — GLP-1 / Consumer Pullback). Two quarters of flat-to-negative US comps would confirm the traffic-loss mechanism and move the weighting from Base toward the structural and recession scenarios.

- Global net unit growth (stores) < 500 (2 consecutive prints → Mid-Cycle — Comps + Unit Growth). Net unit growth below a ~500-per-quarter run-rate would undercut the royalty-base compounding that the Base and Growth scenarios rely on and signal saturation.

- Company-operated / supply-chain operating margin < 0.148 (2 consecutive prints → Traffic Recession — GLP-1 / Consumer Pullback). Consolidated operating margin sustained below the recession-scenario level of 14.8% (versus 15.9% base) would confirm labour and commodity cost pass-through is failing.

- Trailing-twelve-month capital expenditure > 0.17 (2 consecutive prints → Mid-Cycle — Comps + Unit Growth). Capex running above ~$170M against a $130–160M glidepath would signal a build cycle out of step with an asset-light franchisor and pressure incremental ROIC.

- Net-debt-to-EBITDA leverage > 6.0 (single event → Traffic Recession — GLP-1 / Consumer Pullback). A move above ~6x on the securitised balance sheet during a traffic downturn would constrain the buyback that supports per-share compounding and force capital-return retrenchment.

Fact / Inference / Speculation

- FACT: Spot $313; 52-week range $282–$487; engine rating HOLD; base-case target $289 (-8%). (source: Alpha Vantage 2026-06-26, 8 July 2026)

- INFERENCE: Triangulated FV $217 (-31% vs spot · triangulated FV); the rating tracks the Monte-Carlo + scenario-PWEV core; the cash-flow anchor sits below the multiple-discipline core.

- SPECULATION: At current prices the embedded bet is that Gross Margin keeps surprising favourably — an operating call the next two prints will test.

Recommendation: HOLD

Balanced: triangulated fair value $249 (-20% vs spot); the outcome hinges on Gross Margin. The debate is Gross Margin — a fundamental call.

Disclosures & Limitations

This report is for informational and research purposes only. It is not personalised investment advice and does not consider any investor's objectives, financial situation, risk tolerance, tax position, or liquidity needs.

- No suitability assessment has been performed for any individual.

- Market data may be delayed or inaccurate; figures are as of the analysis date.

- Model outputs (fair values, targets, scenario probabilities) are estimates and may be wrong.

- Forecasts are uncertain; past performance is not indicative of future returns.

- The author or publisher may hold positions in securities mentioned.

- Users should verify information against primary sources (company filings) before acting.

- Investing involves risk of loss; there is no guarantee any target price is achieved.

- Ratings follow a defined research methodology (12-month expected-return thresholds), not individual circumstances.